The march toward viable AI use cases

/

John Lin is principal at F-Prime Capital, a global venture capital firm investing in healthcare and technology, with a heritage that spans four decades. Zoey Tang is a former MBA associate at F-Prime Capital.

While artificial intelligence has attracted a lot of interest and investor capital over the last few years, it is by no means a new phenomenon. NVIDIA recently investigated the use of AI in financial services and found it had become “pervasive,” with 75% of financial institutions using at least one of the core accelerated computing use cases, including machine learning, deep learning and high-performance computing.

The fintech industry’s focus on AI, however, has intensified over the last two years, with the advent of consumerized generative AI applications. In our 2024 State of Fintech report, F-Prime Capital delved into the tech industry’s biggest buzzword of the last 12 months to see what effect AI is having in the finance industry, concentrating on the public companies that make up the F-Prime Fintech Index.

Source: F-Prime Capital State of Fintech Report

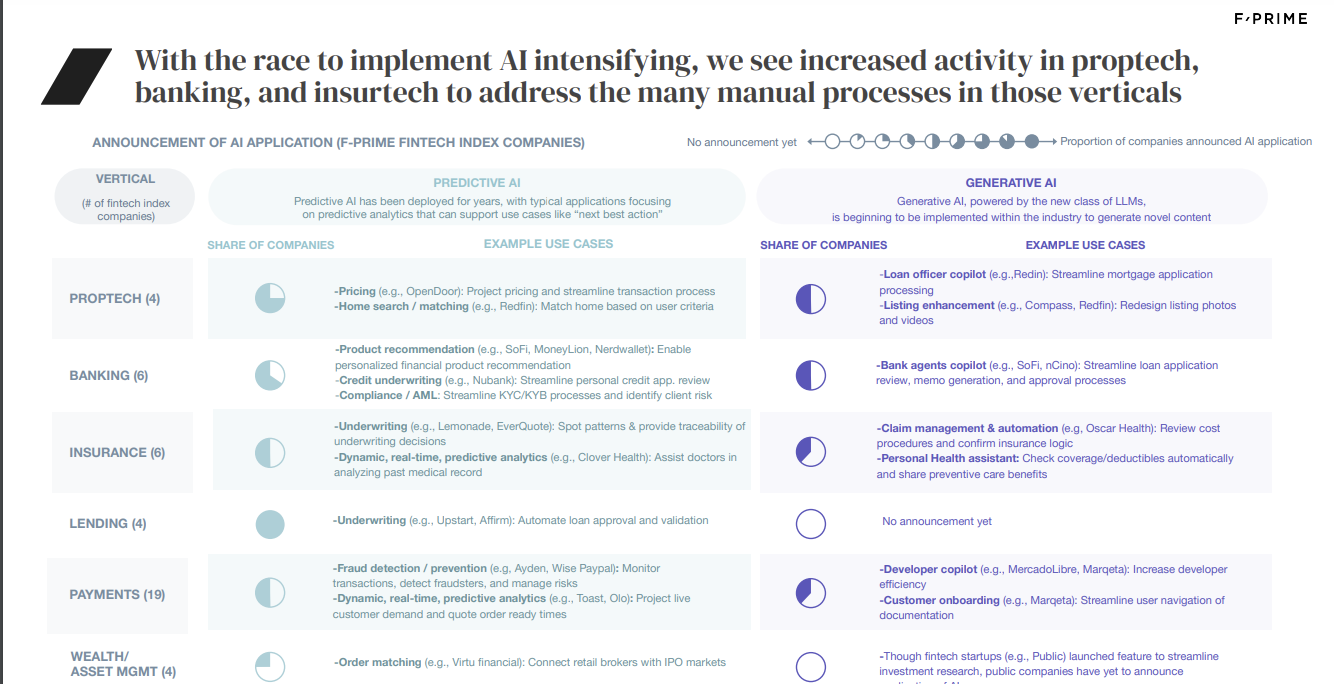

It’s important to distinguish between the two main categories of artificial intelligence: Predictive AI, which has been deployed for years across all financial services sectors, and generative AI, which is still in the early stages of adoption across the industry.

Source: F-Prime Capital State of Fintech Report

Predictive AI

The typical predictive AI application focuses on predictive analytics that can support use cases like “next best action.” Most capital markets, investment banking houses, retail banks and fintech companies are using it to automate repetitive tasks, deliver new products and reduce costs.

Proptech companies like OpenDoor use predictive AI to price projects and streamline transaction processes, and Redfin is leveraging its data to match users to potential homes. Fintech companies like SoFi, MoneyLion and Nerdwallet are using predictive AI to provide personalized product recommendations and streamline KYC processes. AI is also helping banks and neobanks streamline their credit application reviews.

Insurance and lending tech companies are also using predictive AI to help underwrite their products. For example, Lemonade and EverQuote can automatically spot patterns and provide traceability for underwriting decisions, while lenders Upstart and Affirm have automated loan approval and validation processes. Similarly, AI applications at payments companies like Adyen, Wise and PayPal are monitoring transactions to detect fraud. Meanwhile, Toast and Olo are projecting real-time customer demand for stores and predicting the amount of time until an order is ready.

Recently, the rollout of predictive AI has become cheaper and more effective. GPU costs are decreasing and many models require less data to run. What’s more, AI can interpret unstructured documents—including PDFs and emails—broadening the scope of possible use cases.

Generative AI

Generative AI (GenAI) is powered by a new class of large language models (LLMs), and is used to create novel content based on a series of prompts. Though relatively new, finance has been quick to experiment with GenAI and adopt it behind a few use cases. According to NVIDIA research, 43% of respondents are already using it in their organization. Use cases range from internal applications, including yielding investment insights from large datasets. External use cases include personalized banking experiences. For example, Stripe is using GPT-4’s enterprise beta to perform operational tasks like streamlining its UX, triaging customer issues and combating fraud.

Generative AI applications are not yet as widespread in the finance industry as their predictive forebears. In some verticals like wealth and asset management, we have not yet seen any publicly-listed companies on the F-Prime Fintech Index announce GenAI-enabled products or services, though they may be testing them internally. Companies are adopting generative AI applications for low-consequence use cases for now. In the meantime, startups are bringing GenAI to core operations, including, for example, Public’s launch of a GPT-enabled investment “co-pilot.”

So far within financial services, GenAI has had the biggest impact on proptech, banking, and insurtech subsectors, all of which have traditionally relied on manual processes. Proptech and banking companies are using GenAI to start and develop conversations with users through their chatbots. Companies like Redfin and Compass are also redesigning real estate tools, listing photos and videos using GenAI. Banking companies like SoFi and nCino are also generating memos with AI, while insurtech companies’ apps are using AI to review cost procedures and confirm insurance logic, automatically checking customers’ coverage and sharing preventive care benefits.

Mentions of ai in company earning calls

Source: F-Prime Capital State of Fintech Report

Looking Forward

While we are still in the early days of GenAI deployment across the industry, we are seeing signs that financial services companies will continue to invest in this space. Predictive AI is already in wide use throughout the financial services industry, but generative AI will become more popular over the next five years. As AI cuts the cost of financial services and wealth management by automating repetitive tasks, new entrants will need to differentiate themselves with unique offerings like access to alternative assets, lower prices and better customer service. At the same time, these new lower costs will allow new users with lower balances and spending potential to access new kinds of financial services for the first time.